Joint Tenants vs. Tenancy in Common – What You Need to Know When Purchasing a Home!

- Joint Tenancy

- Tenancy in Common

Joint Tenancy

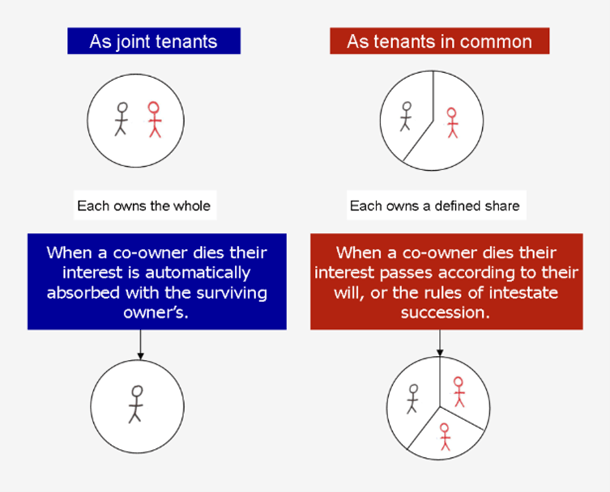

In a joint tenancy, each co-owner holds an undivided interest in the entire property. Together, the joint tenants own 100% of the property — no one owns a specific physical portion.

The Key Feature: Right of Survivorship

The defining characteristic of joint tenancy is the right of survivorship. When one joint tenant dies, their interest automatically passes to the surviving joint tenant(s).

This transfer happens

outside of the deceased’s will and typically does

not form part of the estate for probate purposes (please note probate rules and estate administration taxes vary by province).

As a result:

- A joint tenant cannot leave their interest in the property to someone else in their will.

- The last surviving joint tenant becomes the sole owner of the property.

Who Commonly Chooses Joint Tenancy?

Joint tenancy is often chosen by:

- Married spouses

- Common-law partners

- Some family members

Many couples prefer this structure because it allows property to pass automatically to the surviving spouse without going through probate, potentially saving time and estate administration costs.

However, joint tenancy may not be appropriate in blended families or second marriages, where estate planning goals are more complex.

Tenants in Common

In a tenancy in common, two or more individuals own separate, dividable interests in the same property.

Each owner:

- Holds a distinct share (which can be equal or unequal)

- Still has the right to use and access the whole property

- Can deal with their share independently

Flexible Ownership Shares

Tenants in common can own unequal percentages. For example:

- Owner A: 25%

- Owner B: 25%

- Owner C: 50%

This structure is often used when:

- Co-owners contribute different amounts to the purchase

- Parents co-sign or co-invest with children

- Business partners invest together

- Friends purchase an investment property

Ownership interests can also be acquired at different times.

Estate Planning Implications

Unlike joint tenancy, there is no right of survivorship.

When a tenant in common dies:

- Their share of the property forms part of their estate.

- They may leave their interest in the property to anyone in their will.

- Probate may be required, depending on the circumstances and province.

Each owner may also sell, transfer, or mortgage their share (subject to any co-ownership agreement).

Joint Tenancy vs Tenants In Common

What Happens If the Relationship Changes?

Ownership structure becomes especially important in cases of separation, dispute, or financial difficulty.

Breaking a Joint Tenancy

A joint tenancy can be “severed” (converted into a tenancy in common) if:

- One co-owner transfers or sells their interest

- One owner registers a transfer to themselves as tenant in common (in some provinces)

- A court order severs the joint tenancy

Once severed, the owners become tenants in common.

Ending a Tenancy in Common

A tenancy in common may end if:

- One or more co-owners buy out the others

- The property is sold and proceeds are divided according to ownership shares

- A partition application is brought to court, requesting that the property be sold and proceeds distributed

Former tenants in common may later choose to register as joint tenants if they agree.

Additional Considerations

When deciding how to hold title, consider:

- Estate planning goals

- Blended families

- Creditor protection risks

- Capital gains tax implications (especially for non-principal residences)

- Separation and family law issues

- Contribution amounts and mortgage liability

It is also strongly recommended that co-owners enter into a co-ownership agreement

outlining:

- Financial contributions

- Responsibility for expenses

- Exit strategy

- Dispute resolution

- Buyout terms

This is particularly important for friends, siblings, and investment partners.

Final Thoughts

Choosing between joint tenancy and tenancy in common is not just a technical legal decision — it affects inheritance, taxes, control, and risk exposure.

Before purchasing property with another person, speak with a qualified real estate lawyer to ensure your ownership structure aligns with your financial and estate planning goals.

Mortgages and title structures can be complex — but with the right advice, they don’t have to be - engage an expert.

Kelly Hudson

Mortgage Broker

Mortgage Architects – A Better Way

Mobile: 604-312-5009

Kelly@KellyHudsonMortgages.com

www.KellyHudsonMortgages.com