If you’re buying a condo, townhouse, or bare-land strata property in BC, there’s one document many buyers overlook: the depreciation report. Strata depreciation report requirements - Province of British Columbia And honestly… it’s one of the most important documents you can review before buying. I see this all the time with clients. Some buyers carefully review it. Others quickly skim through it just to “check the box.” But this report can affect: your mortgage approval future repair costs special levies insurance and how stressful ownership may become later So, let’s break it down in simple, real-world language.

Decisions relating to real estate can have significant financial and legal consequences. Before deciding how to share ownership of what is likely one of the largest investments of your life, I recommend consulting a real estate lawyer. Many Canadians purchase property together — including spouses, common-law partners, family members, friends, and business partners. Because ownership structure affects estate planning, taxes, creditor exposure, and control over the property, it’s important to understand your options before you sign. In Canadian property law, there are two primary forms of co-ownership: Joint Tenancy Tenancy in Common While these terms may sound similar, they have very different legal and financial effects — particularly if one owner dies, sells their interest, separates, or faces creditor claims.

If you’re 55 or older and own your home, chances are you’ve heard about reverse mortgages. Sometimes they’re described as a “retirement lifesaver.” Other times they sound risky or confusing. The truth? They’re neither magical nor terrible. They’re simply a financial tool — and like any tool, they work well in some situations and not so well in others – EDUCATION is the key! Let’s break it down in plain English. So… What Is a Reverse Mortgage? A reverse mortgage allows you to borrow money against the value of your home — without making monthly mortgage payments. Instead of you paying the lender every month, the interest gets added to the balance. The loan is typically repaid when: The home is sold You move out permanently Or you pass away In Canada, reverse mortgages are currently offered by: HomeEquity Bank (CHIP Reverse Mortgage) Equitable Bank Bloom Financial You still own your home and your name stays on title. That part often surprises people. How It Works (Simple Version) To qualify: You must be 55 or older You must own your home (you can still have a regular mortgage — it just needs to be paid out) You can usually borrow up to about 55% of your home’s value (the older you are, the more you may qualify for) You don’t make monthly payments. But you must continue to: Pay property taxes Keep home insurance in place Maintain the home The money you receive is tax-free. It can come as: A lump sum Monthly advances Or a combination of both That flexibility is one reason many retirees like this option. Why Do People Consider Reverse Mortgages? Most of the homeowners I speak with aren’t looking for luxury spending money. They’re trying to solve real life situations: Covering rising living costs Paying off debt before retirement Managing health or care expenses Staying in their home longer Helping adult children with a down payment For many Canadians, their house is their largest asset — but it doesn’t create monthly income. A reverse mortgage turns some of that home equity into usable cash. The Pros (The Reasons People Like Them) 1. No Monthly Mortgage Payments This is the big one. If you’re living on CPP and OAS, removing a monthly mortgage payment can dramatically reduce stress. Cash flow improves immediately. 2. You Can Stay in Your Home Most people I meet don’t want to move. They love their neighborhood. Their friends are nearby. Family visits often. A reverse mortgage can allow you to age in place instead of selling before you’re ready. 3. The Money Is Tax-Free Because it’s borrowed money — not income — it does not affect: Old Age Security (OAS) Guaranteed Income Supplement (GIS) That’s a major advantage compared to withdrawing from investments. There are no rules about spending. Some clients use the funds to stay in place – health care at home. Some clients renovate. Some travel. Some gift funds to children. Some simply create a safety cushion. It’s your equity – you decide. 5. You Keep Ownership The bank does not own your home. As long as you live in your home, maintain it, insure it, and pay property taxes — you own your home and can stay. 6. No Negative Equity Guarantee In Canada, reverse mortgages include protection so that you (or your estate) will never owe more than the home is worth — even if property values decline. That protection matters.

What Is BC Assessment? Every January, British Columbia homeowners receive their annual Property Assessment Notice . BC Assessment is a provincial Crown corporation responsible for valuing all real estate in British Columbia for property tax purposes. Each year, BC Assessment provides an estimate of a property’s fair market value as of July 1 of the previous year . 👉 To view the most recent assessment for any property, visit the BC Assessment website and search by address. Important things to understand about BC Assessments Timing matters. Your 2026 assessment reflects an estimated market value as of July 1, 2025, not today. Markets change quickly. In active or volatile markets (like Greater Vancouver and the Fraser Valley), values can shift significantly in a matter of months. Mass appraisal methods are used. BC Assessment relies on algorithms and broad market data rather than a detailed, in-person inspection of your specific home. Because of this, an assessed value can differ — sometimes substantially — from: a lender-ordered mortgage appraisal, or a private real estate appraisal completed for buying or selling. BC real estate context (2026) As we move through 2026, BC housing markets continue to be influenced by: interest-rate expectations and changes by the Bank of Canada, affordability pressures, regional supply constraints, and local economic conditions. This means BC Assessment values should be used only as a starting point , not as a precise indicator of what a property will sell for or what a lender will accept as value. Bottom line: Do not rely on BC Assessment for the exact value of a property you’re planning to sell, purchase or refinance.

Foreign Home-Buyer Tax in BC: What You Need to Know as of Dec. 2025 (For informational purposes only – always confirm details with your accountant & lawyer before buying.)

Buying a home is one of the most important financial decisions you will make and tends to be stressful with all the new terminology. To help you understand the process and have confidence in your choices, check out the following common terms you will encounter during the home buying process. Amortization – Length of time…

Buying a home is one of the biggest financial moves you’ll ever make — and along with it comes a whole lot of new terms, rules, and (you guessed it) insurance . You might think “Mortgage insurance… how complicated can that be?” But once you start hearing about default insurance , mortgage life insurance , and home insurance , it’s easy to get lost in the fine print. Don’t worry — this guide breaks it all d own so you can feel confident about what each type does, what it costs, and why it matters.

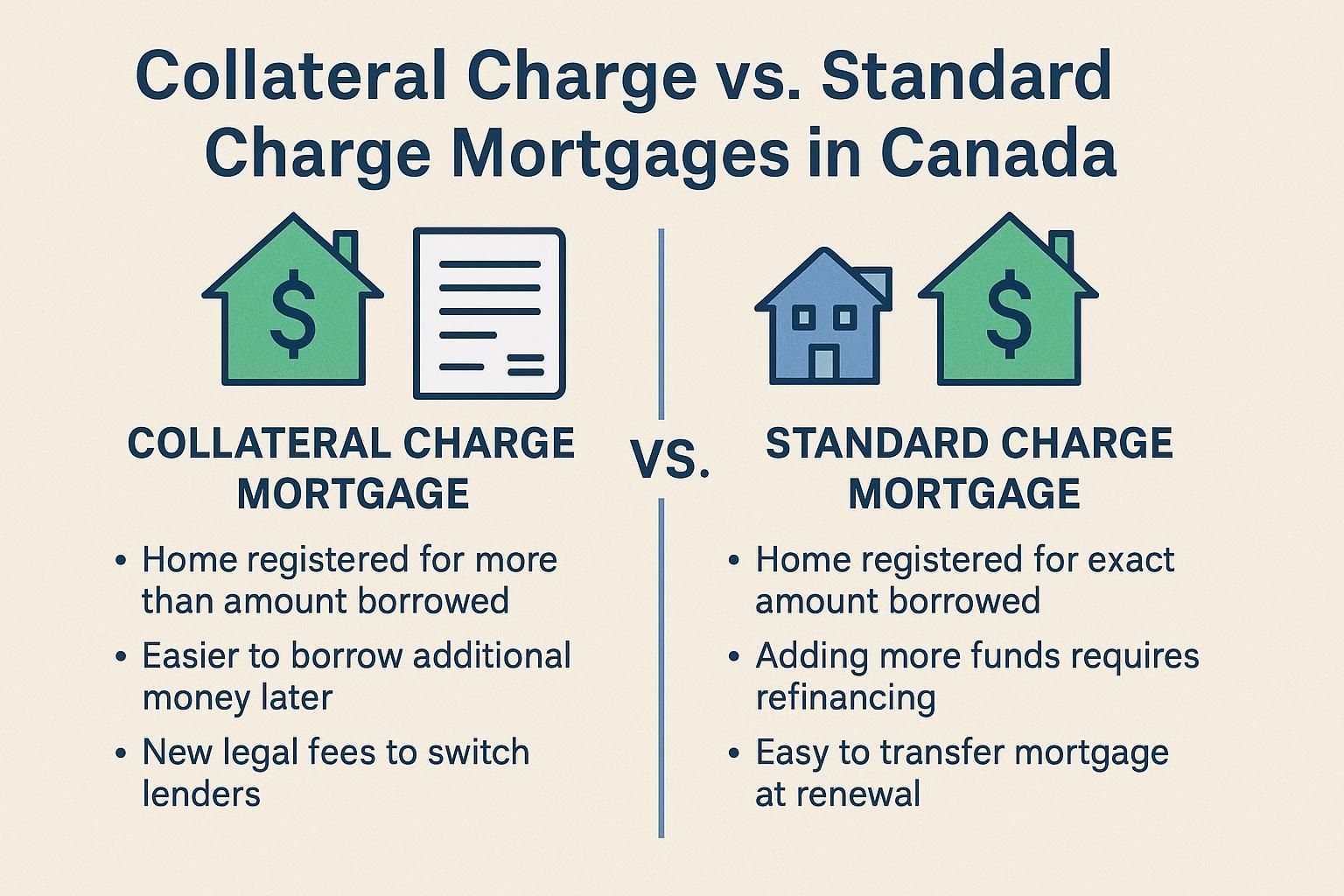

When you’re buying a home in Canada, you’ll hear a lot of new terms. One of those is how your mortgage is registered: as a standard charge or a collateral charge . This choice matters because it affects your flexibility, your costs if you ever switch lenders, and how easy it is to borrow more money later. Let’s break it down in simple terms.

Buying your first home is exciting—and rather nerve-wracking! With so many mortgage options, the process can feel like a maze. My job is to make mortgages simple. Below is your step-by-step guide to how mortgages work , along with the key 2025 updates every homebuyer should know .

British Columbia’s real estate landscape has changed dramatically over the past 15 years. Since 2010, we've seen waves of new legislation, tax policies, zoning reforms, and consumer protections that affect how homes are bought, sold, financed—and lived in. Whether you're a first-time homebuyer or a seasoned investor, keeping up with all these changes can feel overwhelming. That’s why working with a knowledgeable mortgage broker has become more important than ever. Here are 20 key real estate changes in BC since 2010 —and how they affect you.

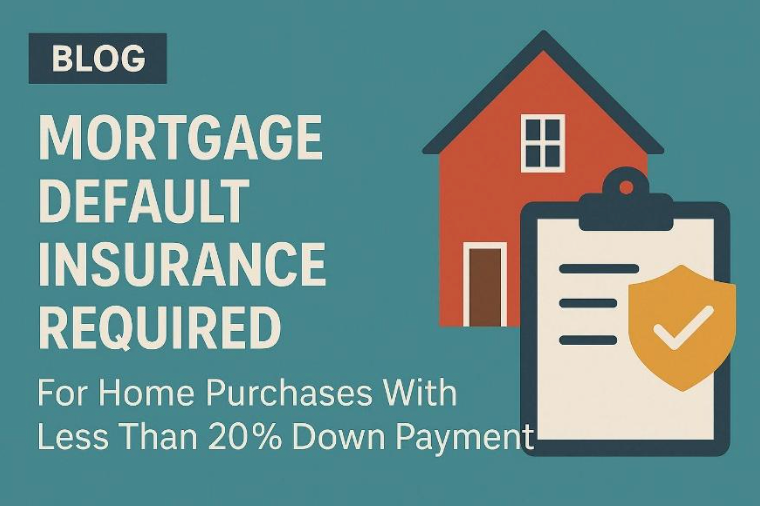

Home buyers say the #1 obstacle to homeownership is saving enough money for a down payment. Mortgage default insurance (also called mortgage insurance) allows you to purchase a home with as little as 5% down . It protects your lender if you stop making payments. Typically, a 20% or higher down payment is your best option. However, for many Canadians, reaching this amount can be challenging, especially in expensive markets like Greater Vancouver & Toronto. If you don't have enough cash for a 20% down payment, Mortgage Default Insurance can help. How Much Down Payment Do You Need?

Have you ever dreamed of buying a piece of land and building your very own home from scratch? You're not alone! Buying bare land, especially in beautiful British Columbia, Canada, can be an exciting adventure or a money pit. Before you start dreaming of where to put your future house, there are a few important things you should know. What is Bare Land? Bare land, sometimes called vacant land, is just that—land without any buildings or structures on it. It's an empty canvas waiting for your ideas. But buying bare land isn’t quite the same as buying a house or apartment. It comes with its own set of rules and challenges, especially when it comes to financing. Why is Financing Bare Land Different? When you buy a home, Lenders feel safer lending you money because if something goes wrong, they can sell the house to get their money back. With bare land, it’s different because there’s nothing built yet. It’s harder to sell bare land – than a home. Which makes it riskier for Lenders, therefore they usually have stricter lending rules and higher interest rates to offset the risk. Important Things to Consider About Financing Bare Land: 1. Down Payments Can Be High Raw Land : This is completely untouched land without any utilities like water, sewer, electricity, or roads. Lenders often require a large down payment, sometimes around 50% of the land’s price. Due to the higher perceived risk, many lenders do not lend on raw, undeveloped land. Vacant or Serviced Land : This land already has important utilities (like electricity, water, sewer, gas, telecommunications, and road access) nearby or already installed. Because it's easier to build on, Lenders may require a slightly lower down payment, usually around 35%. 2. Higher Interest Rates and Shorter Loan Terms Interest rates on land loans are generally higher than on regular home loans because of the increased risk. Also, Lenders might offer shorter loan terms. Some lenders may offer loans where you only pay interest for a few years, which can help lower your monthly payments in the short term. 3. Finding the Right Lender There are three main places to get a land loan: Traditional Banks : Major banks sometimes provide land loans but usually with strict rules, high down payments, and higher interest rates. Credit Unions : Local credit unions can often have more flexible rules and may offer better terms, especially if the land is within their local lending area. Private Lenders : Companies specifically dealing with land financing. They offer customized loans but typically charge fees for borrowing the money and higher interest rates.

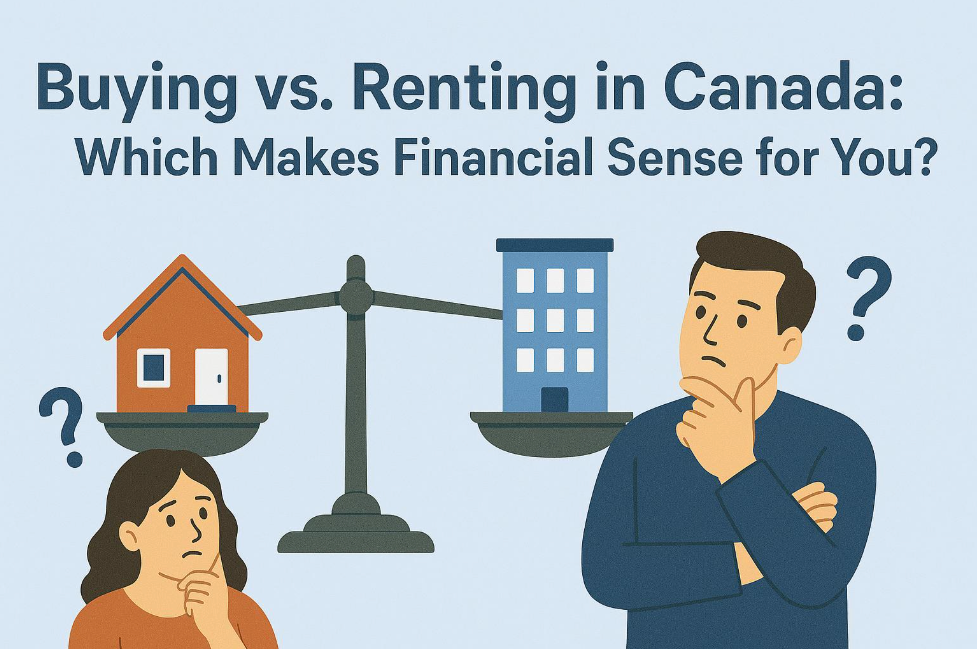

Are you debating whether it's smarter to rent or buy a home in Canada? It's a common question, and the answer depends on your personal situation. Both renting and buying have their pros and cons, but for most people, homeownership tends to offer substantial long-term benefits. Let’s explore both options clearly, so you can confidently decide what’s best for you. Advantages of Buying a Home 1. Personal Freedom and Customization Owning your home means having the freedom to personalize your living space. Dreaming of a bold paint colour or unique flooring? Go ahead—your home, your rules! 2. Building Equity and Wealth Each mortgage payment you make is an investment in yourself. Over time, your home typically appreciates in value, increasing your equity. This can become a significant asset that helps secure your financial future. 3. Stability and Security Owning offers peace of mind. You don’t need to worry about sudden rent hikes or eviction notices. Your home remains yours until you decide otherwise. 4. Long-Term Financial Benefits Homeownership acts as forced savings. Unlike renting, every mortgage payment moves you closer to outright ownership, building a financial foundation that can support you and your family for years to come. Challenges of Buying a Home 1. Upfront Costs Buying comes with significant initial costs, including a down payment, legal fees, home inspection, appraisal, moving expenses, etc. 2. Responsibility for Maintenance Owning a home means you're responsible for maintenance and repairs. This can sometimes be costly and inconvenient. 3. Reduced Flexibility Selling a home typically takes time, which can limit your flexibility if you need or want to relocate quickly. Advantages of Renting 1. Easy Mobility Renting offers flexibility to relocate easily, beneficial for frequent job changes or lifestyle adjustments. 2. Fewer Responsibilities Repairs and maintenance are generally your landlord’s responsibility, reducing stress and unexpected expenses. 3. Lower Initial Costs Renting typically requires just a security deposit and the first month's rent, making it easier financially at the start. Downsides of Renting 1. No Equity Building Rent payments do not contribute to your equity. Instead, you’re effectively paying your landlord’s mortgage, offering no long-term financial return. 2. Restrictions and Rules Landlords often impose limitations, such as no pets or restrictions on decorating, making it challenging to feel fully at home. 3. Instability and Uncertainty Renters may face sudden rent increases or eviction if the landlord decides to sell or repurpose the property, disrupting your life significantly.

Since March 2022, mortgage rates in Canada have risen significantly, raising concerns for homeowners and potential buyers. But what drives these changes, and how do they impact your choice between fixed and variable mortgage rates? Let's simplify this important financial topic.

Separation and divorce are major life events that significantly impact finances—including homeownership. In Canada, approximately 40% of marriages end in divorce , making it a common challenge for homeowners. As a mortgage broker, I work with many clients who are navigating the challenges of keeping or selling their home, refinancing, or qualifying for a new mortgage post-separation. Lenders assess these applications differently than standard ones, particularly when it comes to income, debts, and liabilities . Whether you want to stay in your current home or move on to a new one, understanding your mortgage options is essential. How Separation & Divorce Impact Your Mortgage When separating from a spouse, one of the biggest financial decisions is what to do with the family home. Here are some common scenarios: 1. Keeping the Home If one spouse wants to stay in the home, they must refinance the mortgage to remove the other person’s name from title and buy out their ex’s share of the equity. 2. Selling the Home In some cases, selling the home and splitting the proceeds is the best financial option. This provides a clean break but requires both parties to qualify for new mortgages if they wish to buy separate homes. 3. Co-Owning After Separation Some ex-partners choose to co-own the home for a period, often for the sake of stability for children. While this may work temporarily, it will complicate future borrowing power . 4. Existing Mortgage Responsibilities Even if a separation agreement states that one party is responsible for the mortgage, lenders will still consider both parties liable unless the mortgage is refinanced and the ex’s name is removed from the title & the mortgage. Important : If both names remain on the mortgage and your ex stops making payments, your credit score and future borrowing ability will be affected .

What is BC Assessment? It’s January and in BC homeowners are receiving their property assessments. BC Assessment is a provincial Crown corporation that values all real estate property in British Columbia. Every year, BC Assessment sends property owners a Property Assessment Notice telling them the fair market value of their property as of July 1 the prior year . To see the most recent assessment for a property, click on BC Assessment and type in the property address. The real estate market is the single biggest influence on market values. Market forces vary from year to year and from property to property. The market value on an assessment notice may differ from that shown on a bank mortgage appraisal or a real estate appraisal because BC Assessment’s appraisal reflects the value as of July 1 of 2024 , while a private appraisal can be done at any time. The assessed values are based on limited information and are a result of algorithms and mass appraisal techniques which have their limitations. BC in general A new report forecasts the average price of B.C. home in 2025 at just over $1 million — the highest in Canada, some $280,000 above the national average. These figures appear in the latest forecast from the Canadian Real Estate Association released Jan. 15, 2025. Factors The increase in home prices was driven by a decrease in fixed mortgage rates and expectations for future Bank of Canada rate cuts. Use your BC Assessment as a starting point for the value of the property you’re planning to purchase… Do not rely on BC assessment for the exact value of the property you’re considering purchasing. Markets in BC change quickly both increasing and decreasing in value depending on the area and the economy.

48% of Canadian homeowners are 55+ and many find that their homes represent a significant portion of their net worth. For retirees looking to access their home equity without selling or moving, a Canadian reverse mortgage offers an ideal solution. However, this financial product isn’t without its complexities.

On September 24, 2024, the federal government announced expanded parameters for lenders and mortgage default insurers to begin offering insured mortgages as of December 15, 2024. The expanded parameters include: expanding the eligibility for 30-year amortizations and increasing the $1 million purchase cap to $1.5 million. Eligibility for 30-year amortizations for insured mortgages To qualify for the 30-year amortization: the loan to value must be 80% or higher; and the borrower must be a first-time homebuyer OR purchaser of a new build. There is a premium of 0.20% on the 30-year amortization

There seems to be some confusion about what it means to co-sign on a mortgage… and any time there is confusion about mortgages, it’s time to chat with Kelly Hudson, your trusted mortgage expert!! Thanks to tighter mortgage qualification rules and higher-priced real estate - particularly in the greater Vancouver and Toronto areas - it is not easy to qualify for a mortgage on your own merits. Let’s look at why you would want to have someone co-sign your mortgage and what you need to know before, during, and after the co-signing process. The ‘stress test’ has been especially “stressful” for borrowers. As of Jan. 1, 2018, all homebuyers need to qualify at the rate negotiated for their mortgage contract PLUS 2% OR the government posted rate which varies (as of Oct. 2024 5.25%), which ever is higher . If you have less than 20% down payment, you must purchase Mortgage Default Insurance and qualify at 5.25%. If you must qualify at a rate higher than what you are paying… then your money doesn’t go as far… and you qualify for a smaller mortgage. In the wise words of Mom’s & Dad’s of Canada… “if you can’t afford to buy a home now, then WAIT until you can!!” BUT wait… in some housing markets (especially Vancouver & Toronto), waiting it out could easily mean missing out, depending on how quickly property values are appreciating in the area you want to purchase. If you can’t income qualify for a mortgage with your current provable income along with GREAT credit, your lender’s going to ask for a co-signer. In order to give borrowers, the best mortgage rates, Lenders want the best borrowers!! They want someone who will pay their mortgage on time as promised with no hassles. Co-sign vs Guarantor Short version: The main difference between a guarantor and a co-signer is that the co-signer is a title holder and a guarantor is not. However, both individuals are responsible for mortgage payments being made to the lender. Someone can co-sign your mortgage and become a co-borrower , the same as a spouse or anyone else who you are buying the home with. It’s basically adding the support of another person’s income and credit history to those initially on the application. The co-signer will be put on the title of the home and lenders will consider them equally responsible for the debt should the mortgage go into default. Another option is a guarantor . If a co-signer decides to become a guarantor, then they’re backing the loan and essentially vouching for the person getting the loan that they’re going to be good for it. The guarantor is going to be responsible for the loan should the borrower go into default. Most lenders prefer a co-signer going on title. More than one person can co-sign a mortgage although it’s typically the parent(s) or a close relative of a borrower who steps up and is willing to put their neck, income, and credit bureau on the line. Ultimately, if the lender is satisfied that all parties meet the qualification requirements and can lessen the risk of their investment, they’re likely to approve your mortgage. Before signing on the dotted line Short Version: A co-signer, in essence, co-owns the home with the individual living in it and paying the mortgage. A co-signer must sign all the mortgage documents and their name will appear on the title of the property. When you co-sign on a mortgage, you become just as responsible for the mortgage loan as the primary borrower — and you can suffer serious consequences if they make late payments or default. Anyone that is willing to co-sign a mortgage must be fully vetted, just like the primary applicant(s). They will have to provide all the same documentation as the primary applicant(s). Being a co-signer makes you legally responsible for the mortgage, exactly the same as the primary applicant(s). Please note as a Co-signer your future borrowing plans will be affected Since the mortgage will also appear on your credit report, this additional debt could make it tougher for you to qualify for additional credit down the road. For example: if you dreamed of one day owning a vacation home, just know that a lender will have to consider 100% of your co-signed mortgage as part of your overall debt-to-income ratio . You are allowing your name and all your information to be used in the process of a mortgage, which is going to affect your ability to borrow anything in the future. If the Co-signer already owns a home, then they could be charged capital gains on the property they co-signed for IF the property sells for more than the purchase price (contact your accountant for tax advice). In Canada, capital gains tax is charged on the profit made from selling real estate, including homes, for more than their purchase price. However, there is an exemption for primary residences. If the home was your primary residence for the entire period of ownership, you are generally exempt from paying capital gains tax on the sale. A primary residence is where you or your family lived most of the time, and only one property per family can be designated as such per year. This gets complicated for co-signers – since they rarely live in the home they are co-signing for. For non-primary residences, (rental, investment properties, co-signed properties) capital gains tax applies to the profit made from the sale. In Canada, the CRA taxes 50% of gains up to $250,000, and 66.7% of gains over $250,000. For example, selling a rental property that you purchased for $300K and sold for $400K would result in a $100K capital gain. Typically, we’ll put the co-signer(s) on title for the home/mortgage at 1% of home ownership... then IF there were a capital gain, they would pay 1% of their share of the capital gain (contact your accountant for tax advice). If someone is a guarantor , then things can become even trickier as the guarantor isn’t on title to the home. That means that even though they are on the mortgage, they have no legal right to the home itself. If anything happens to the original borrower, where they die, or something happens, they’re not on the title of that property but they’ve signed up for the mortgage. The Guarantor doesn’t have a lot of control which can be a scary thing. In my opinion, it’s much better for a co-signer to be a co-borrower on the property, where you can be on title to the property and enjoy all the legal rights afforded to you. The Responsibilities of Being a Co-signer Co-signing can really help someone out, but it’s also a big responsibility. When you co-sign for someone, you’re putting your name and credit on the line as security for the loan/mortgage. If the person you co-sign for misses a payment, the lender or other creditor can come after you to get their money. Any late mortgage payments would also show up on your credit report, which could impact your own loan/mortgage qualification in the future. Because co-signing a loan has the potential to affect both your credit and finances, it’s extremely important to make sure you’re comfortable with the person you’re co-signing for. You both need to know what you’re getting into. I recommend Independent Legal Advice between all co-borrowers. Co-signing is NOT a life sentence. Just because you need a co-signer to get a mortgage does not mean that you will always need a co-signer. In fact, as soon as you can credit & income qualify for the mortgage on your own (without your co-signer) – you can ask your lender to remove the co-signer from title. It is a legal procedure so there will be a cost associated with the process, but doing so will remove the co-signer from your mortgage loan and release them from the responsibility of your mortgage. Removing a co-signer technically counts as changing the mortgage, so you need to ensure that the lender you chose doesn’t consider removing a co-signer (changing the covenant) as breaking your mortgage. There could be large penalties associated with doing so. For more information, check out my BLOG Mortgage Penalties – Ouch… How Much??